Match Group (MTCH) – Long-Term Investment Analysis

Article 2 of this weeks series on social media

Note: If you are interested in stock write-ups, I also wrote pitches or stories about St. Joe Co., TSLA, Reliance Industries, BRK.B, ETH, and the Alternative Asset Managers.

Investment Thesis and Overview

Match Group (NASDAQ: MTCH) appears undervalued relative to its historical multiples and peers and is positioned to resume solid long-term growth through product innovation and international expansion. Despite recent headwinds (flat revenue growth in 2023-24 and Tinder’s user plateau), Match generates robust free cash flow, enjoys high returns on capital, and owns the world’s leading dating app portfolio. At ~14× earnings and an ~11% free cash flow yield, near multi-year lows, the market is pricing in very low growth. However, with initiatives to reinvigorate Tinder engagement, the rapid international growth of Hinge, and expansion in underpenetrated markets like Asia, Match Group has the levers to compound earnings in the coming 5+ years. We recommend a bullish long-term stance, expecting that improving growth and sustained capital returns (including a new dividend) will drive significant shareholder value. Key catalysts include a potential re-acceleration of revenue in 2024-2025, margin expansion from efficiencies, and sizable share buybacks, while risks to monitor are intensifying competition and execution challenges in new markets.

Valuation and Financial Metrics

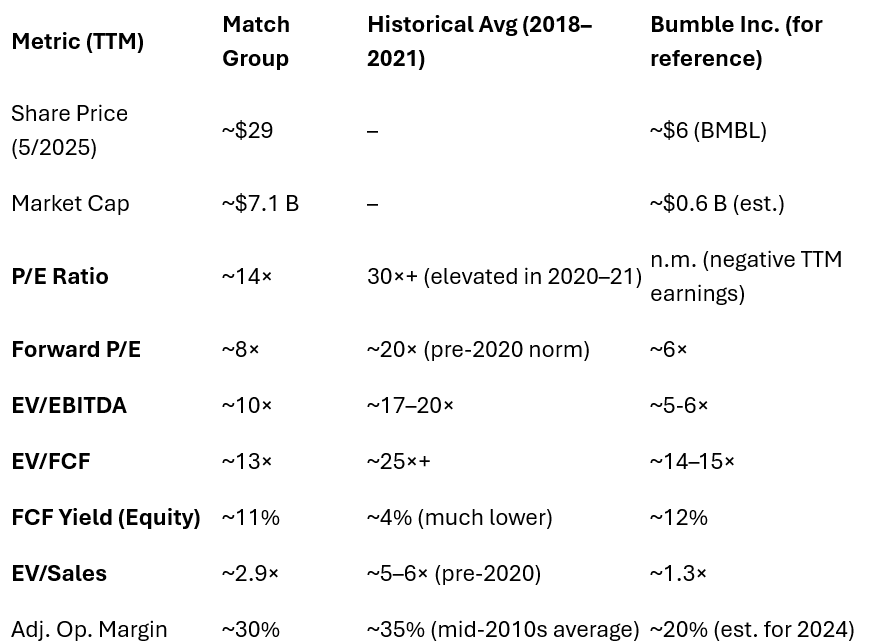

Match Group’s current valuation is historically low, reflecting recent growth challenges but also offering a favorable entry point if fundamentals improve. Core valuation metrics are attractive relative to the past and to peers:

Free Cash Flow Yield: Match generates strong free cash flow thanks to its asset-light model. The stock’s FCF yield is ~11–12% on the current market cap, a dramatic increase from the low single-digit yields (~3–4%) at its peak valuation a few years ago. In other words, Match trades at only ~9× trailing free cash flow, which suggests a high “shareholder yield” if cash flows are sustained or grow. Even on an enterprise basis, EV/FCF is ~13× now, versus ~32× in 2021.

EV/Sales: The stock’s EV is only about 2.9× TTM revenue, down from an EV/Sales above 13× in 2021. With a 33% adjusted operating margin as of Q1 2025, Match’s current price implies an attractive <3× EV/sales for a high-margin franchise.

Peer Comparison: Major rival Bumble Inc. (BMBL) trades at even lower absolute multiples (recently ~5–6× EV/EBITDA and ~0.6× P/S) due to its own growth slowdown. However, Bumble’s profitability is lower and its user base smaller. Match’s P/E is roughly in line with Bumble’s ~9× forward P/Egurufocus.com, but Match boasts higher margins and far greater free cash flow. Moreover, Match’s FCF yield (~11%) is comparable to or better than Bumble’s (mid-teens)financecharts.com, indicating that both dating app leaders are out-of-favor. Match’s scale and diversified brands arguably warrant a premium, yet it currently can be bought for a similar or lower multiple than Bumble – a compelling valuation discrepancy.

To illustrate Match Group’s valuation in context, below is a summary of key metrics:

Table: Match Group’s valuation metrics vs. historical levels and Bumble. Match now trades at a significant discount to its historical valuation, and roughly on par with or cheaper than Bumble on many metrics despite a stronger market position. This conservative pricing provides a margin of safety if Match’s earnings simply remain flat – and considerable upside if the company returns to growth.

Growth Drivers and Long-Term Opportunities

Match Group’s ability to compound capital over 5+ years will depend on reigniting revenue growth. Key drivers include:

Tinder Product Reinvigoration: Tinder is the flagship, contributing ~55% of Match’s revenue. Lately Tinder has seen declining users and revenue (-7% YoY in Q1 2025), as product stagnation and competition weighed on engagement. Management is aggressively addressing this. Tinder’s new CEO has unveiled a roadmap of innovations – focusing on authenticity, improved matching via AI, and new features to make the app “fun” again. Upcoming additions like mandatory photo verification (to boost trust), an AI-driven matchmaking algorithm, and even a “double dating” feature (letting friends pair up for group dates) aim to re-energize Tinder’s user growth. Tinder still boasts 47 million monthly users globally and extremely strong brand recognition, so even modest improvements in conversion of free users to payers or ARPU can move the needle. Pricing power is another lever – Tinder has introduced higher-priced tiers (e.g. Tinder Platinum) and à la carte features in recent years, demonstrating it can raise revenue per user without massive user growth. If Tinder stabilizes and returns to low-single-digit growth (through new features and better Gen Z appeal), it will provide a solid foundation for Match’s overall revenue.

Hinge – High Growth & International Expansion: Hinge is Match’s rising star. Marketed as the app “designed to be deleted” (i.e. focused on serious relationships), Hinge has been on a tear with ~23% YoY revenue growth as of Q1 2025 and ~19% user (payer) growth. Quarterly Hinge revenue hit $152M in Q1’25 (nearly 20% of total revenue), and its operating margins are improving (now ~19% on a GAAP basis, 28% adjusted) as it scales. Hinge has built strong positions in core Western markets (U.S., U.K., Canada, Australia) and has expanded into continental Europe, where it now ranks among the top 2 dating apps in many countries. Further international rollout is a catalyst: Match is actively localizing Hinge for non-English markets and plans to launch it across Asia and other regions. Given Hinge’s success with “intentional daters,” these expansions could fuel high double-digit growth for years. Management projects Hinge can reach $1 billion in revenue by 2027, roughly tripling from current levels – a bold target that underscores Hinge’s importance in the growth story. To achieve this, Hinge is leveraging Match’s extensive data and AI capabilities (e.g. new AI-driven recommendations and coaching features) to improve user experience, which should drive retention and monetization. In sum, Hinge is likely to be a key compounder within Match Group, offsetting Tinder’s maturation.

International & Asia Expansion: Outside of North America and Europe, online dating adoption is still in early innings, offering Match a long runway abroad. In particular, Asia ex China represents a huge opportunity: online dating penetration is only ~7% in Asia (vs. much higher in Western markets). Cultural norms have historically favored offline or family-arranged matchups in parts of Asia, but this is changing rapidly as younger generations turn to apps. Match Group has reorganized to seize this opportunity – it created a dedicated MG Asia division with region-specific apps and strategies. One success story is Pairs (a Japanese app in the Match portfolio), which leads Japan’s serious dating segment and is credited with 10% of all marriages in Japan. Pairs is now expanding to other Asian markets, using features like AI-based “Real Mind Match” compatibility tests tailored to local cultures. Elsewhere, Match’s 2021 acquisition of Hyperconnect gave it products like Azar, a live video chat app popular with Gen Z. Azar is gaining traction across Asia and beyond as a more social, real-time way to meet people. Monetizing such “social discovery” apps could unlock new revenue streams beyond traditional swipe apps. Although Match Group’s Asia segment is currently small (~8% of revenue) and faced an 11% YoY revenue drop in Q1 2025, it did grow payers by 5% in the region – suggesting user uptake is happening even if monetization (or FX) lagged. Over a 5-year horizon, we expect Asia to turn into a growth engine as localization improves. Even capturing a single-digit percentage of the massive singles population in markets like India, South Korea, and Indonesia could contribute meaningful incremental revenue. Demographic trends favor this expansion: emerging markets have large, young populations increasingly delaying marriage and adopting smartphones – fertile ground for dating apps.

Broader Demographic Tailwinds: Globally, the pool of potential online dating users continues to expand. Social norms around meeting online have shifted – in the U.S., over 40% of couples met online by the late 2010s (up from ~20% a decade prior), and that figure exceeded 50% by 2021 in some surveys. Younger generations use dating apps as a default; more than half of Americans under 30 have tried online dating. As millennials and Gen Z age into prime single years (and older age groups grow more comfortable with technology), the total addressable market of online daters grows. Additionally, people are marrying later and a higher share of adults are unmarried than in past decades, which extends the years individuals might use dating apps. These secular trends should provide a tailwind of user growth or at least sustained demand for matchmaking services over the next 5+ years. Match Group, with its broad portfolio (from casual apps like Tinder to niche community apps like BLK/Chispa to relationship-focused Hinge/Match.com), is well placed to capture a large slice of new users entering the online dating world.

In summary, while Match’s recent top-line growth has been muted (2024 revenue grew only 3% YoY and early 2025 is slightly down), the company has clear avenues to reaccelerate growth: revitalizing Tinder, scaling Hinge globally, and tapping underpenetrated markets. Even moderate success in these initiatives – for example, low-double-digit growth in Hinge and Asia, and flat-to-positive Tinder growth – could sustainably push Match Group’s overall revenue growth back into the high single digits or low teens annually. Given management’s focus (they cite targeting 10%+ CAGR longer-term2), we see a path for Match to compound revenue and earnings at a healthy rate over a 5-year horizon.

High Margins and Capital Efficiency (ROIC/ROE)

Match Group’s business model shows excellent capital efficiency and profitability, supporting its ability to compound capital:

Strong Margins & Cash Generation: Match operates a collection of digital platforms, which have high incremental margins. Its operating margin is around 20% in recent quarters, and Tinder’s margin is even higher (42% operating margin in Q1’25). The company converts a large portion of operating profit into free cash flow. With minimal capital expenditures (typically <$70M/year) and modest working capital needs, Match’s free cash flow margin has hovered around 25% or more. In 2024, Match generated ~$882M of free cash on ~$3.48B revenue (~25% FCF margin), and FCF should rise if growth and cost efficiencies improve. These healthy cash flows not only provide funds for growth investments but also support shareholder returns (dividends and buybacks).

Returns on Invested Capital (ROIC): By virtue of its asset-light profile, Match boasts high returns on capital employed. ROIC is consistently around 17–18%, which is well above the company’s cost of capital. Notably, this ROIC is calculated including goodwill from acquisitions; the core return on tangible capital is much higher. This level approaches the lower end of tech giants (for example, Alphabet at ~30%+ ROIC) and far exceeds many smaller internet peers that struggle to break into double-digit returns. High ROIC suggests Match can continue to invest in expansion (or acquisitions) and earn good returns, compounding value internally. While ROICs are reasonable, the profitability of the company is a victim of it’s own success. The better MTCH pairs people into relationships, the faster people churn off the site. This has been a problem with Tinder, as the company admitted marketing spend to bring in new customers had be deprioritized after the pandemic, preventing the company from replacing churned customers. For the foreseeable future, higher marketing spend will be needed to combat the apps success.

Overall, Match’s profitability profile – high margins, strong free cash conversion, and high ROIC – underpins its capacity to self-fund growth and return excess cash. This is a hallmark of a good long-term compounder, as it can grow without dilutive capital raises and can enhance per-share results via buybacks/dividends.

Competitive Landscape

Match Group enjoys a leadership position in the online dating industry but faces competition from both established rivals and new entrants:

Bumble: Bumble (NASDAQ: BMBL) is the second-largest publicly listed dating company and Match’s most direct competitor in Western markets. Bumble’s main app (Bumble) is known for its women-message-first feature, appealing to female users. Bumble has grown rapidly since its 2014 founding, reaching ~$0.9–1.0B in annual revenue and about 2.7 million payers – but growth has recently stalled (Q1 2025 revenue fell ~6% YoY). Bumble’s strengths include strong brand awareness among young adults and a diversifying product (it also offers friend-finding and networking modes). However, Bumble operates essentially two apps (Bumble and Badoo) vs. Match’s many, and Bumble’s profitability (~20% EBITDA margin) trails Match’s (~33%). Notably, Bumble’s user base is smaller (around 40 million active users) and skews more toward specific regions (North America and Europe). Match’s Tinder remains the far larger global platform, with ~10 million payers vs. Bumble app’s ~2.3 million payers in 2024. While Bumble will remain a formidable competitor – especially in markets like the U.S. and UK where it has strong footing – it is unlikely to displace Tinder’s scale. Match’s multi-brand strategy also provides a buffer: someone leaving Bumble might end up on Hinge or Tinder, both owned by Match. Indeed, Hinge directly competes with Bumble for “relationship-minded” singles, and its rapid growth (23% YoY) outpacing Bumble’s suggests Match is successfully capturing that segment. The competitive rivalry with Bumble will continue to necessitate marketing spend and innovation (for example, Bumble has copied features like profile badges and Tinder has answered by emphasizing safety features), but overall Match’s breadth and head start give it a resilient edge.

Private and Regional Players: Apart from Bumble, there are numerous private or regional dating apps. In the U.S., Grindr (focused on LGBTQ+ dating) is a notable player; while Grindr went public via SPAC, it remains much smaller in revenue and caters to a specific niche. Match has its own entrant for this segment (Archer, a new app for LGBTQ users), but Grindr’s strong network effect in its niche means it will coexist. eHarmony and Coffee Meets Bagel are other long-standing dating services (private) focusing on serious matchmaking; they have loyal user bases but significantly less scale and marketing reach than Match’s apps. Internationally, local apps are prominent in certain countries: for example, in China, apps like Tantan (owned by Hello Group/Momo) and Baihe serve millions since Western apps are restricted – Match has little presence in China due to regulatory barriers, effectively ceding that market. In Japan and East Asia, several domestic apps (e.g. Omiai, EastMeetEast) compete, but Match’s Pairs is a leader in Japan. In India and Southeast Asia, where arranged marriage culture intersects with modern dating, local startups (such as Shaadi.com for matrimony or Tinder’s local clone apps) attempt to capture users. The competitive moats in dating are moderately strong: network effects (people go where the profiles are), brand trust (especially around safety and success rates), and continuous innovation are key. Match’s scale gives it a data advantage – its apps collectively have 82 million monthly users generating 5 billion data points a day, which can feed better AI matching algorithms than smaller rivals can develop. Moreover, Match’s diversification means it covers many niches (demographic or interest-based dating communities), making it harder for a new entrant to offer something entirely novel. That said, competition is dynamic and low in switching costs – users often use multiple apps and can shift if an app offers a better experience. A potential disruptive threat could come from a new format (for example, a TikTok-style video dating app or an AI matchmaker bot) that captures young users’ attention. Match is hedging this by investing in new formats itself (video-based apps like Azar, and AI features across products).

Social Media and Other Platforms: It’s worth noting indirect competition from social networks and other meeting avenues. Apps like Instagram, TikTok, or Meetup aren’t dating apps per se, but young people do meet and form relationships through them. Facebook Dating was launched by Meta as a free service integrated into Facebook. However, to date Facebook Dating has not significantly impacted the leaders – it lacks the focus and user mindset that dedicated dating apps foster. The fact that a giant like Meta entered dating and hasn’t dethroned Match is a testament to the incumbents’ advantage in this space. Still, big tech remains a latent threat given their resources (for instance, if Meta or another player decided to aggressively invest in a standalone dating service or acquire a competitor). So far, regulatory hurdles (antitrust concerns would likely prevent Meta from buying Match) and strategic focus elsewhere have limited this threat.

In summary, Match Group’s competitive position is strong but not unassailable. It leads a duopoly with Bumble in many markets, with Match holding the larger share. A plethora of smaller rivals nibble at niches, and new apps can always emerge, but achieving scale is difficult due to network effects. Match’s strategy of broad brand portfolio and continuous innovation is aimed at defending its moat. We believe this approach will keep Match the dominant player, though it will need to execute well (e.g. ensure Tinder doesn’t lose relevance, and Hinge continues to thrive) to fend off rivals. Competitive pressures are partly why Match’s growth slowed – it can’t be complacent – but thus far the company has shown an ability to either acquire threats (it bought Hinge when it was up-and-coming) or outcompete them with its resources.

Why Are Metrics Under Pressure? – Qualitative Insights

To fully evaluate Match as an investment, one must understand why some recent financial metrics have weakened and whether those issues are cyclical or structural:

User Engagement & Growth Patterns: The pandemic era (2020–21) saw a surge in dating app usage (people stuck at home turned to virtual connection) and then a subsequent normalization. Tinder in particular benefited in 2020, but by 2022–23, its user growth stalled. Some of Tinder’s struggles have been self-inflicted – product missteps and leadership churn in 2022 led to slower feature rollout and a weaker value proposition for users. This manifested in flat or declining payer counts (Tinder payers -6% YoY in Q1 2025). Additionally, as Tinder’s core North American demographic matures, it has had difficulty attracting Gen Z users who seek more varied, authentic experiences than the swipe model. These issues explain why Tinder’s growth and revenue per user metrics stalled recently. The upside is that they appear fixable with renewed focus on product and marketing (as described in the growth drivers section). We are already seeing small positive signs, such as Tinder’s revenue per payer (RPP) ticking up 1% and total RPP for Match Group up slightly in Q1 2025, indicating pricing improvements.

Subscription vs. Ad Model and Monetization: Match Group primarily monetizes via subscriptions and in-app purchases (boosts, super-likes, etc.), not advertising. This has pros and cons. The subscription model yields high margins and steady cash flow (recurring revenue from millions of subscribers), but it requires constant delivery of value to keep users paying. If users feel they can achieve similar results on a free app or free tier, they may cancel subscriptions. Over 2022–2023, subscription growth slowed as the value proposition lagged – for instance, Tinder Gold’s features became familiar and perhaps less enticing over time. Match is addressing this by adding new premium features and tiering (e.g., introducing an ultra-premium tier for power users willing to pay more). Pricing power has generally been strong (Match has regularly raised prices or introduced higher-priced options without mass churn, showing a loyal segment of users). We expect monetization per user to continue rising, especially as new features (like priority recommendations, profile boosts, etc.) roll out – but this must be balanced against not driving users away with too many paywalls. On the advertising front, Match has started experimenting (Tinder has some ads in the free experience), which could become a modest secondary revenue stream. However, ads are unlikely to overtake subscriptions in the near future, given dating apps’ usage patterns and privacy concerns.

Regulatory and Platform Risks: Match has had disputes with mobile app stores over fees – notably it sued Google over Play Store billing policies. Google and Apple’s 30% commission on in-app purchases is essentially a tax on Match’s revenue. Any changes in that regime (for example, legal/regulatory changes forcing lower fees or allowing third-party billing) could boost Match’s margins. Conversely, tighter regulations on data use or online interactions could impose new costs. In various jurisdictions, dating services face scrutiny related to user safety (e.g., verifying ages, preventing harassment and scams). Match has invested in safety features and moderation, but a serious incident could bring reputational or legal risks. So far, it has managed to generally stay ahead of regulation by self-policing (e.g., ID verification features, background check partnerships). Another consideration: privacy laws (like GDPR in Europe) restrict data usage – since Match leverages user data for matching algorithms, it must ensure compliance, though this hasn’t been a major issue so far. Overall, regulatory factors haven’t materially hurt Match’s financial metrics yet, but they remain an area to watch (for instance, if an age-verification law required costly implementation, or if app store policies shift unpredictably).

Why margins fluctuated: We saw Match’s operating income margin dip in some years (e.g., 2022’s op income fell even as revenue rose)stockanalysis.com. This was due to rising costs – the company significantly ramped R&D and marketing, especially for new brands and features (like video and AI initiatives), and incurred higher compensation expense (including stock comp) post spinoff. Additionally, acquisitions like Hyperconnect added cost structure. By 2023, Match began realizing efficiencies: it reduced duplicative functions and slowed hiring, helping op margins recover somewhat. Going forward, management’s plan to centralize tech infrastructure and share resources across brands should yield cost savingsmtch.com. We anticipate modest margin expansion over the next few years as revenue growth returns and these efficiency moves pay off – on top of the natural high incremental margins of digital services. Already in Q1 2025, despite lower revenue, adjusted operating margin was a robust 33% due to cost disciplineinvesting.com. Thus, the recent margin compression appears cyclical and addressable, rather than a permanent decline in business economics.

In essence, Match’s recent financial softness (low growth, slight margin dips) can be traced to product-cycle issues at Tinder, increased competition, and investment cycles, rather than a terminal decline in demand. These are challenges one expects in a maturing market but ones that Match is actively mitigating. The qualitative analysis suggests that with renewed focus, the core usage and engagement can be improved, which should translate back into healthier financial metrics (re-accelerating revenue and stable or growing margins).

Risks and Challenges

No stock is without risks. Key risks to the Match Group thesis include:

Execution Risk on Turnaround: The biggest internal risk is that Tinder’s refresh efforts might underwhelm. If new features fail to significantly improve the user experience or if competitors replicate them quickly, Tinder’s user base could continue to erode. Given Tinder’s outsized share of profits, further slippage would drag overall results. Similarly, Hinge’s expansion might hit hurdles – cultural missteps in new markets or simply slower uptake outside anglophone countries could mean Hinge’s growth falls short of lofty expectations. The strategy of pushing AI and new features needs to translate into user engagement; execution missteps (as happened in 2022 with a now-scrapped Tinder venture into the “metaverse” and virtual currency that wasted resources) can set back growth. We will monitor app store rankings, user reviews, and payer trends for signs that execution is on track.

Competitive Pressure and Innovation: The competitive landscape discussed could intensify. Bumble is not standing still – it continues to market heavily and could innovate in ways that appeal to users (for instance, Bumble has been developing features around communities and platonic connections that keep users in its ecosystem longer). If Bumble or a new entrant captures a trend (say, a shift to video dating or a viral dating format) faster than Match, it could siphon users. The risk is particularly pronounced with younger Gen Z users, who can be fickle and flock to new social apps quickly (as seen with phenomena like TikTok). Match must balance adapting to trends with not alienating existing users. Network effect moats can be eroded if a challenger achieves critical mass – not easy, but possible in the tech world. A related risk is user fatigue: some users might simply tire of swipe apps, leading to a secular stagnation in dating app usage. Match’s portfolio approach (different apps for different preferences) is a hedge, but if the overall consumer interest in app dating waned, it would hurt all players.

Macro and Demographic Risks: Our thesis leans on favorable demographics and more singles using these apps. It’s possible that in some markets the addressable single population actually shrinks (e.g. countries with declining young population or unexpectedly higher marriage rates). Economic factors could also play a role – while dating apps are not very expensive, prolonged economic hardship might reduce people’s willingness to pay for subscriptions, especially if free alternatives exist. So far, the business has been relatively resilient (dating demand is somewhat non-cyclical; people seek partners in good times and bad), but it’s not immune. A period of high inflation could push Match to raise prices, which might spike churn if not coupled with added value.

Regulatory/Safety Issues: If a high-profile safety incident occurs (for example, a crime associated with a dating app meeting), it could invite regulatory crackdowns. Match has faced lawsuits in the past regarding screening of users. Stricter rules (like mandated ID verification for all users or liability for user interactions) could increase costs or friction to user sign-up. Privacy regulation is another area: if laws limit use of personal data or communications mining for matching algorithms, it could reduce the effectiveness of Match’s services. International regulations in new markets might also pose hurdles – for instance, some countries have data localization laws or content requirements that apps must meet. Any compliance failures could result in fines or app store removals.

Despite these risks, we believe Match’s risk/reward is favorable at the current valuation. The company has navigated challenges before (e.g., overcoming the entry of Facebook Dating, integrating acquisitions) and still grown. Key will be agile product execution and maintaining user trust – areas where Match is investing heavily (in AI, in safety, etc.). Our thesis would be undermined if growth stays persistently near zero or negative, implying that dating apps have peaked or Match is losing share. In that bearish scenario, the stock might remain a value trap despite low multiples. However, given the fundamental human need for connection, ongoing cultural shifts toward online matchmaking, and Match’s assets, we see a low probability of stagnation that cannot be reversed.

Conclusion – Long-Term Outlook (Bullish)

We conclude that Match Group is an attractive long-term investment (5+ year horizon) given its combination of a discounted valuation, dominant market position, and multiple avenues for renewed growth. At ~$29 per share, the stock reflects a pessimistic view that recent struggles will persist indefinitely. Our analysis suggests otherwise: Match has the tools to re-accelerate growth – Tinder’s refresh, Hinge’s expansion, and tapping Asia’s potential – which in turn should drive earnings higher and likely re-rate the stock to higher multiples. Even under conservative assumptions (mid-single-digit revenue CAGR and stable margins), Match’s EPS could grow double-digit percentages annually for the next few years (helped by buybacks), supporting a much higher share price. The company’s high ROIC and robust free cash flow generation indicate a business that can fund its own growth and enrich shareholders simultaneously.

Q1 2025 segment performance highlights Match Group’s mixed near-term trends: Tinder’s revenue fell 7% YoY while Hinge grew 23% YoY, and smaller brands/regions declinedinvesting.cominvesting.com. Tinder still produces hefty profits (42% op margin)investing.com, but to resume overall growth Match relies on Hinge and new markets to pick up the slack. This snapshot underscores the short-term headwinds (Tinder slowdown) against the long-term opportunities (surging Hinge, untapped Asia), reinforcing the need for strategic execution.

Over a 5+ year span, we expect Match Group to compound value through a mix of moderate organic growth, high profit retention, and shareholder-friendly capital allocation. By 2030, online dating will likely be even more culturally entrenched worldwide, and Match’s brands (especially Tinder and Hinge) should remain at the forefront of facilitating connections. If the company achieves even a portion of its targets (e.g. Hinge hitting $1B revenue by 2027, Tinder returning to growth, Asia doubling penetration), Match’s financial profile in five years could be materially larger – and the market would no longer justify only ~10× forward earnings for such a business. We see a plausible scenario where Match’s stock delivers strong returns (outpacing the broader market), driven by EPS growth and multiple expansion from these depressed levels.

In conclusion, Match Group is a compelling long-term play on an enduring human trend (the quest for love/companionship, increasingly mediated by technology). The company has proven resilient and adaptable in the past, and its current strategy addresses its weaknesses while capitalizing on its strengths. Investors at today’s valuation are essentially getting a high-cash-flow franchise at a bargain price, with a free call option on re-accelerated growth via new innovations. While vigilance is required on execution and competitive risks, the balance of evidence – from core valuation metrics to growth drivers – supports a bullish investment thesis: go long Match Group for the next five years.

If you want to read an even more in-depth article, I encourage you to look at Bristlemoon’s analysis.

Note: This is my own opinion and not the opinion of my employer State Street or any other organization. I do not own MTCH but may trade in and out of any stock at any time. This is not a solicitation to buy or sell any stock. My team and I use a Large Language Model (LLM) aided workflow. This allows us to test 5-10 ideas and curate the best 2-4 a week for you to read. Rest easy that we fact-check, edit, and reorganize the writing so that the output is more engaging, more reliable, and more informative than vanilla LLM output. We are always looking for feedback to improve this process.

Additionally, if you would like updates more frequently, follow me on x: https://x.com/cameronfen1. In addition, feel free to send me corrections, new ideas for articles, or anything else you think I would like: cameronfen at gmail dot com.